When we plan our future, we prepare for the worst in advance, right? Then why should we take a mortgage in a different way?

If you have a mortgage or you’re planning on getting one, the stress test is one way of preparing for the worst.

What is the Mortgage Stress Test?

Despite its name, a mortgage stress test is not a test. We could define as a way to determine if the applicant is and will be able to keep up with their payments even if the interest rate change.

For that reason, you will need to qualify at your quoted rate mortgage interest rate plus 2% or the Bank of Canada’s five-year benchmark rate.

At this point, you might be wondering why we need the stress test, but the answer is really simple, it exists to protect borrowers like you. The government wants to make sure you’ll still be able to afford your mortgage payments even if rates eventually go up. Think about it this way; if you couldn’t afford higher payments in the future, you could be forced to default on your mortgage and lose your home.

When was the Stress Test Established?

The Canadian Mortgage Stress Test was introduced in 2018 by the federal government. Anyone applying or renewing a home loan must undergo this test; even those who are putting a minimum down payment of 20%.

Important note: The past 12th of August 2020, the BOC rate went down to 4.79%.

How does it work?

When applying for a mortgage, you’ll be offered a quoted rate; however, the lender would like to make sure that you can still pay your mortgage if rates increase.

There are 2 different ways for the lender to check if you are capable to make payments:

The Bank of Canada qualifying rate of 4.79%

Your quoted rate + 2%

You’ll usually need to be able to qualify for the higher of the two rates. This means that if you want to be able to pay down your mortgage at a higher price, your income has to be high enough, and your existing debt if you have it has to be low enough.

For those home buyers that already have a mortgage but want to renew it, they’ll only need to “pass” the stress test if switching lenders.

How to use CMA Stress Test Calculator

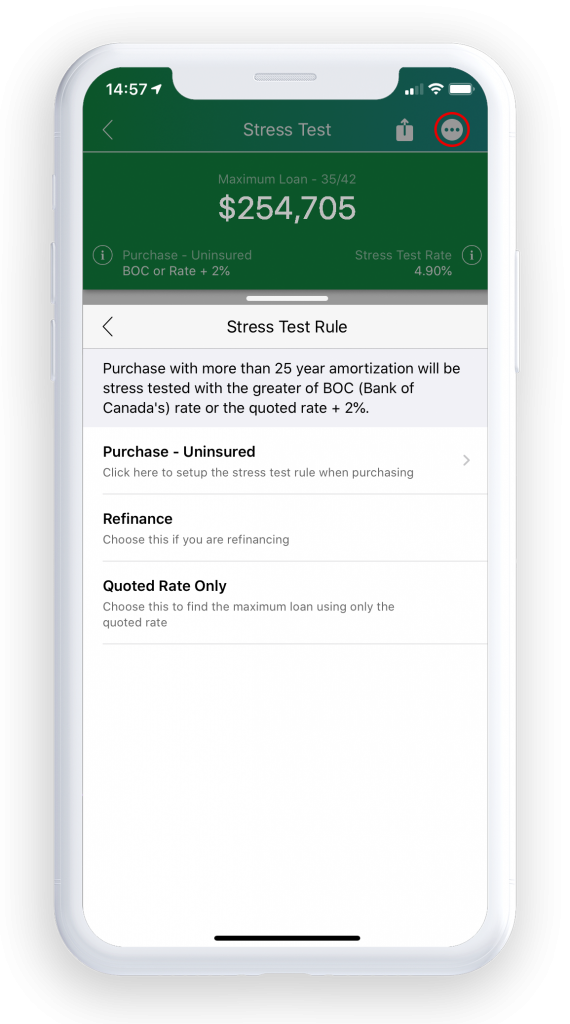

1. Where to find it

On the main screen, look for the card titled “Stress Test”.

2 Stress Test Tool Options

Tap on the top right corner to access the options menu, and before you start putting your information, make sure that you have the right options set in, such as:

Purchasing a house over 1 million.

Downpayment over 20%

Amortization period over 25 years.

Refinance if you are refinancing your home.

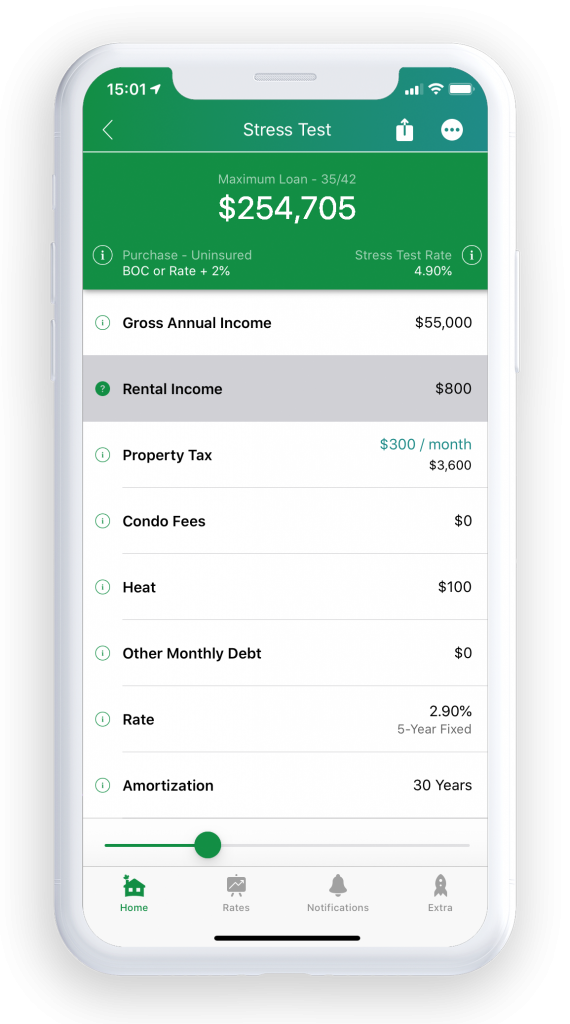

3 Enter your Information

Gross Annual Income

Rental Income if you are planning on renting the property

Property taxes

Condo fees, if you are buying a condo

Heat

Monthly debt if you have it

Rate

Amortization

As a homebuyer is essential to know all the Canadian mortgage regulations because they will directly impact your mortgage. And if you want to increase the amount that you can borrow, our advice is to either increase your income or save more money for a down payment.

If you have more questions about all these regulations or you want to get pre-approved, click on the link below to get in contact with the best mortgage broker around you.

Make a request to speak to a mortgage professional